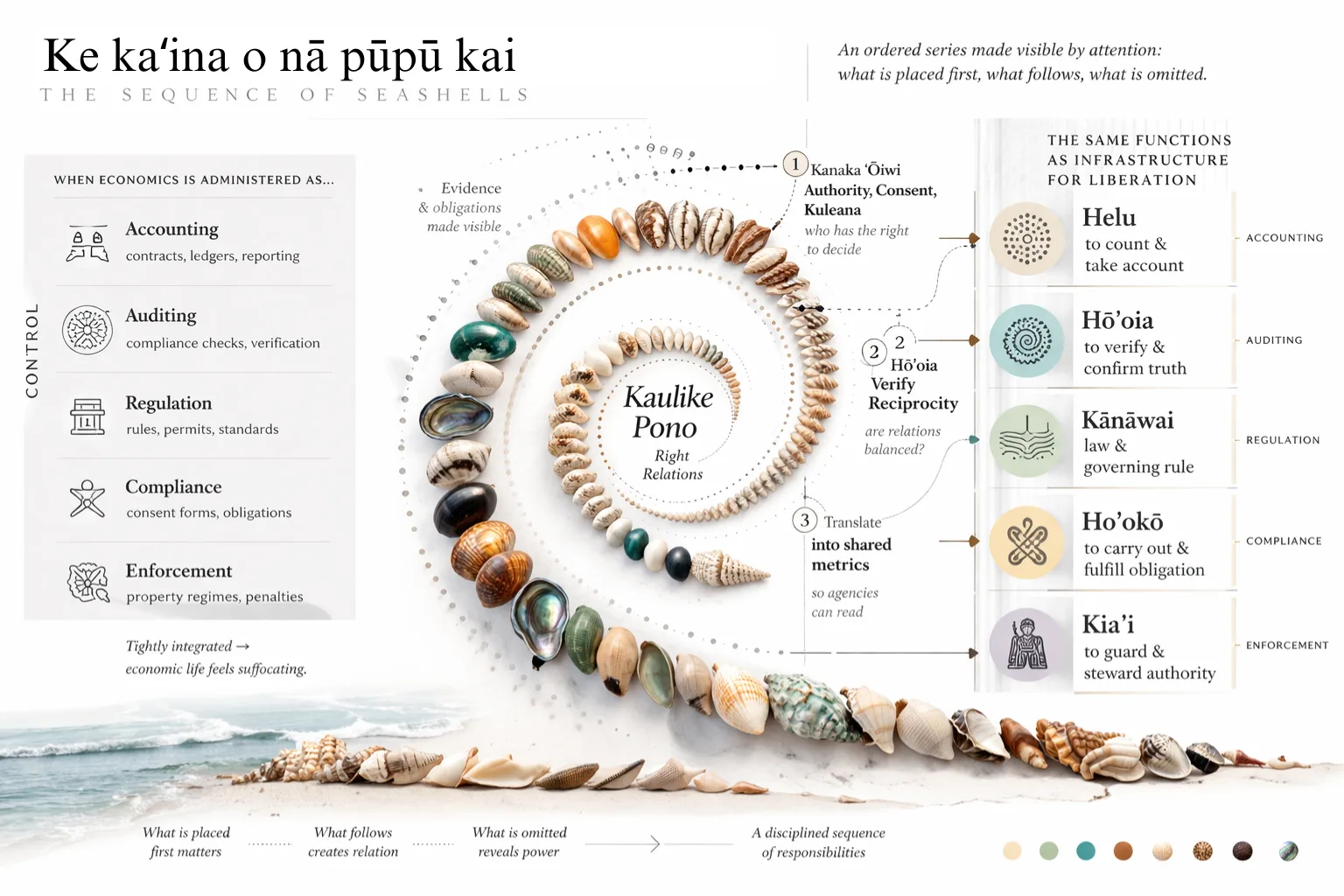

A Field Guide to Institutional Capture, Cooptation, and the Erasure of Transformative Frameworks

As a follow up to the Black Paper, this document describes patterns by which institutions — including multilateral bodies, NGOs, certification systems, and government agencies — publicly embrace transformative frameworks while systematically hollowing them out. The examples are drawn from REDD+, organic certification, fair trade, biodiversity offsets, indigenous data sovereignty frameworks, and other fields where the gap between stated intent and operational reality is well-documented.

I think we’ve all witnessed these scenarios first hand and as we unpack this further, we can see how corporations normalize our slow erasure by capture culture .

“The most dangerous capture is the kind that arrives wearing the language of the thing it is replacing.“

The Anatomy of Institutional Capture

Institutional capture looks like enthusiasm followed by very slow, very technical adjustments that each seem reasonable in isolation. By the time the original framework is unrecognizable, those who built it have been incorporated into the structure that consumed it — often as advisors, consultants, or working group members who are now invested in defending what replaced their original vision.

Asset stripping, financial engineering, and value extraction– the dismantling or good business practice by vulture investors– may just be what investors learn in top-tier business schools, as the mechanics of what Eddie Lampert did to Sears has now become textbook.

The following examples are drafted so that we can manage our expectations as we consider what it means to create intermediaries across many multiple sectors.

The Enthusiastic Embrace

Institutional adoption often begins with public endorsement. Senior leaders reference a new framework in speeches, policy documents, strategic plans, and funding announcements. The framework’s originators are invited to conferences, highlighted in communications, and recognized for their contributions. At this stage, broad agreement is easy because the framework remains defined at a high level of generality.

The more significant questions emerge later when governance, standards, funding, and implementation are established. Early endorsement can create the appearance of alignment before these questions have been resolved. Institutions may begin incorporating the framework’s language into existing programs, policies, and initiatives, suggesting continuity between the new framework and established practice. Meanwhile, the individuals and communities that developed the framework often occupy visible symbolic roles without possessing equivalent influence over how it is defined, administered, or applied. Recognition and authority become increasingly separated, with the former arriving well before the latter.

| The Enthusiastic Embrace | Observable Signal | Mechanism | Seen In |

| Embrace | Vague high-level endorsement; framework language in existing program descriptions | Institution claims ownership of concept before governance is settled; defines who gets to define it | REDD+ — World Bank endorsed ‘forest peoples’ language while structuring Forest Carbon Partnership Facility to route through national governments |

| Embrace | Original authors invited to speak but not to govern | Visibility without power; the community legitimizes the institution’s claim without gaining structural control | Organic certification — USDA invited early organic farmers to advisory panels while the National Organics Standards Board authority was progressively narrowed |

Technical Annexation, aka the Standards Process

Standardization is often presented as a necessary step for expanding a framework beyond its original context. Institutions establish working groups, commission experts, and develop operational definitions intended to make concepts measurable, comparable, and administratively manageable. The stated objective is consistency, credibility, and wider adoption.

In practice, the standardization process often privileges forms of knowledge that institutions already know how to measure, audit, and regulate. Quantitative indicators, technical methodologies, and established reporting systems gain prominence because they fit existing administrative structures. Knowledge rooted in relationships, local context, oral traditions, or community practice is frequently deferred, simplified, or treated as supplementary.

Participation by the originating community may continue throughout the process, but decision-making authority increasingly shifts toward those with technical expertise, regulatory influence, or institutional standing. Individual compromises can appear modest when considered separately. Taken together, they can gradually redefine the framework in ways that align it more closely with institutional requirements than with its original purpose.

| Technical Annexation | Observable Signal | Mechanism | Seen In |

| Standards | Technical working group formed; community originators are minority | Standards are built around instruments the institution already controls; qualitative knowledge is deferred | REDD+ safeguards — Cancun Safeguards (2010) acknowledged indigenous rights but deferred measurement to national governments with no binding mechanism |

| Standards | ‘Pragmatic compromises’ on core mechanisms, each presented as minor | Cumulative redirection toward institutional legibility; each compromise seems reasonable until the architecture is unrecognizable | Fair Trade — FLO’s 2011 decision to allow large-scale plantations under Fair Trade label fundamentally altered the small-farmer-cooperative model |

The Certification Hustle

Certification often emerges as a mechanism for ensuring consistency, accountability, and public trust. Over time, however, the certification process can become a separate source of authority. Recognition depends less on participation in the originating community and more on compliance with standards defined, interpreted, and enforced by external institutions. The ability to navigate audits, documentation requirements, legal procedures, and certification fees becomes increasingly important.

As this process develops, barriers to participation tend to rise. Small-scale practitioners, subsistence communities, and locally governed initiatives may struggle to meet administrative and financial requirements that were not designed around their circumstances.

Larger organizations with greater resources are often better positioned to secure certification and expand under the framework’s banner.

Appeals and governance processes frequently remain within the institutions that administer certification, limiting community influence over how standards evolve. The result is a gradual shift in authority from the communities that developed the framework toward the organizations responsible for managing, verifying, and scaling it..

| The Certification Hustle | Observable Signal | Mechanism | Seen In |

| Certify | Certification costs prohibitive for small-scale practitioners | Scale advantage for commercial actors; framework label migrates to the actors it was designed to constrain | Organic — By 2010, USDA Organic was dominated by large agribusiness; small farmers faced compliance costs averaging $1,000–$5,000/year |

| Certify | Appeals route through the certifying body | Community has no independent recourse; the gatekeeper adjudicates challenges to its own gatekeeping | Gold Standard carbon credits — third-party auditors are paid by project developers, creating structural conflict of interest in verification |

| Certify | Certifying body revenue depends on certification volume | Structural incentive to lower rather than maintain standards over time | Marine Stewardship Council — documented cases of fisheries receiving certification despite scientific consensus on stock depletion |

Market Absorption as Shitification

Market absorption occurs when a framework attracts investment, institutional support, and pressure to expand. Growth brings visibility and resources, but it also changes what the framework must become in order to move across large organizations, regulatory systems, and financial markets. Elements that can be standardized, audited, compared, and reported are elevated. Elements rooted in local context, community authority, and place-specific relationships become more difficult to accommodate and gradually lose influence.

The transition is often described as maturation, professionalization, or scaling. Success is increasingly measured through aggregated indicators that demonstrate growth across regions, sectors, or portfolios while obscuring local variation and unintended consequences.

Practitioners entering the field learn the institutionalized version as the accepted model and may never encounter the original debates, objectives, or constraints. Those who continue to raise concerns about what has been lost are often characterized as unrealistic, resistant to change, or attached to an earlier stage of development. The result is not necessarily the abandonment of the framework, but its adaptation to the requirements of the systems that adopted it.

| Market Absorption | Observable Signal | Mechanism | Seen In |

| Scale | ‘Maturing’ and ‘professionalizing’ language; original architects described as purists | Normalization of the captured version; critique is reframed as anti-progress | REDD+ — By 2015, World Bank literature described early community-consent concerns as ‘implementation challenges’ rather than design requirements |

| Scale | Success metrics aggregated nationally/globally; local divergence invisible | Community-level failure is averaged out; perverse outcomes are statistically masked | Biodiversity Net Gain (UK) — habitat units aggregated across sites allow habitat destruction in high-value locations offset by lower-value gains elsewhere |

| Scale | New entrants learn only the scaled version | Original framework intent disappears from institutional memory within one professional generation | Fair Trade USA — split from FLO (Fair Trade Labeling Organization) in 2011 and moved toward ‘Fair Trade Certified’ for large farms; the next generation of practitioners knows only this version |

Entrenchment

Entrenchment occurs when organizations absorb criticism without changing their underlying practices. Critical research and alternative perspectives may be acknowledged, but they are treated as peripheral to the work that institutions consider important or practical. Calls for reform are often directed into review processes, advisory groups, or consultations that can discuss problems but lack the authority to address their causes. Over time, the appearance of engagement replaces meaningful change, allowing existing structures, incentives, and assumptions to remain intact.

| Entrenchment | Observable Signal | Mechanism | Seen In |

| Entrench | Critical literature acknowledged but described as ‘not operationally relevant’ | Academic critique is absorbed and neutralized; it proves the institution is reflective without requiring change | Carbon markets generally — IPCC and academic literature on permanence and additionality problems are widely cited in institutional documents while market structures remain unchanged |

| Entrench | New frameworks met immediately with embrace | The cycle restarts; the institution is now experienced at rapid conceptual absorption | Nature-based Solutions — within 18 months of gaining traction, NbS had been endorsed by the same institutional actors whose carbon market practices it was designed to critique |

Case Studies in Detail

REDD+ — The Forest That Became a Financial Instrument

REDD+ (Reducing Emissions from Deforestation and Forest Degradation) began as a mechanism to keep forests standing by compensating countries for avoided deforestation. The original proposal, from Papua New Guinea and Costa Rica at COP11 in 2005, was built on the principle that forest communities should be the primary beneficiaries.

What happened: The World Bank’s Forest Carbon Partnership Facility, established in 2008, routed all REDD+ finance through national governments. The Cancun Safeguards of 2010 required countries to ‘promote and support’ indigenous rights but created no binding measurement, reporting, or verification mechanism for whether rights were actually upheld. By 2015, multiple independent assessments found that less than 1% of REDD+ finance had reached local communities. The framework’s language — ‘community consent,’ ‘benefit sharing,’ ‘safeguards’ — remained intact while its operational structure systematically excluded the communities it named.

The specific mechanism: Governments were made the unit of accountability, and governments had sovereign authority to define what ‘adequate consultation’ meant. The community consent principle was real in the text and absent in practice because the verification mechanism was controlled by the party whose behavior it was meant to constrain.

Organic Certification — The Capture of a Movement

The organic farming movement emerged from the 1970s as a critique of industrial agriculture — not merely a set of input restrictions but a philosophy of soil health, community food systems, and farmer autonomy. The USDA National Organic Program, established under the Organic Foods Production Act of 1990, took seven years to implement and was the product of sustained industry lobbying that progressively narrowed the original framework.

What happened: The NOSB (National Organic Standards Board) was established with farmer and consumer representation, but its recommendations became advisory rather than binding. The ‘Big Three’ exemptions — hydroponics, confined animal feeding operations, and synthetic materials added through the National List — each represented a fundamental departure from the original framework’s intent. By 2020, the largest ‘organic’ operations bore no resemblance to the farming philosophy that created the label. The label had been successfully separated from the practice.

The specific mechanism: Compliance was defined in terms of inputs (what you don’t use) rather than outcomes (what the farm produces ecologically). This made large-scale operations compliant by default — they could meet input restrictions at scale — while the relational, soil-health, and community dimensions of organic practice, which were the original framework’s core, had no measurement mechanism and therefore no certification pathway.

Fair Trade — The Plantation Problem

Fair Trade emerged from Nicaraguan coffee cooperatives in the late 1980s as a mechanism for small-scale farmer cooperatives to access premium markets with guaranteed minimum prices. The cooperative model was not incidental — it was the financial instrument. Cooperatives captured the premium collectively, distributed it through democratic governance, and used it to fund community infrastructure.

What happened: Fair Trade USA’s 2011 split from Fairtrade International (FLO) was precipitated specifically by the question of whether large-scale plantations employing wage labor could be certified. Fair Trade USA argued that certifying plantations would dramatically increase volume and market penetration. FLO refused. Fair Trade USA proceeded independently and now certifies plantation-grown products under the same label that the cooperative movement created. In some commodity categories, the majority of ‘Fair Trade’ volume now comes from sources that the original framework was designed to compete against.

The specific mechanism: The label was separated from the governance model. Once a product label can be earned through compliance with input standards (minimum wage, working conditions) rather than ownership structure (cooperative), the economic power the framework was designed to redistribute stays with the same actors. Workers on a certified plantation earn more than they otherwise might. They do not own the cooperative.

Indigenous Data Sovereignty — The Platform Problem

Indigenous data sovereignty frameworks — including the CARE Principles and the work of the Global Indigenous Data Alliance — assert that indigenous communities have the right to govern data about their peoples, lands, and cultures. The principles are well-developed, internationally endorsed, and increasingly cited in government and institutional data policies.

What is happening now: The institutional response has been to create ‘indigenous data portals’ and ‘community data platforms’ — typically hosted on infrastructure owned by universities, government agencies, or NGOs. Communities are invited to upload their data to these platforms, to set access permissions, and to govern what is shared. The data sovereignty principle is operationally present. The data itself is on someone else’s server, under someone else’s terms of service, in a jurisdiction the community does not control.

The specific mechanism: Sovereignty is enacted at the permission layer while ownership is quietly transferred at the infrastructure layer. This is the most technically sophisticated form of capture precisely because it produces documentation — access logs, consent records, governance protocols — that appear to demonstrate compliance with the data sovereignty principle while the underlying architecture makes genuine sovereignty structurally impossible.

Protective Architecture — What Prevents Capture

No framework is capture-proof. But certain structural decisions dramatically increase resistance. The following principles are drawn from the cases above — specifically from what the original frameworks either lacked or lost during their capture.

Governance Before Standards

The community that originates a framework must control the governance body before any standards process begins. If the institution controls the working group, it will control the outcome regardless of who else is in the room. Governance membership, quorum rules, veto rights, and amendment procedures must be established in community-controlled form before any invitation to ‘collaborate on standards’ is accepted.

Infrastructure Sovereignty, Not Just Permission Sovereignty

Data sovereignty, measurement sovereignty, and financial sovereignty require owning the infrastructure, not just controlling the permissions layer on someone else’s infrastructure. This is expensive and technically demanding, but it is the only form of sovereignty that survives institutional engagement over time. Permissions can be renegotiated. Infrastructure ownership requires negotiation to transfer.

Community Recall Over Intermediary Roles

Any intermediary role — certifier, translator, data steward, financial agent — must be subject to community recall without destroying the instrument the intermediary was managing. If removing an intermediary requires unwinding the financial or certification structure, the intermediary has de facto captured the community’s dependency. Recall mechanisms must be designed in advance, before the financial value of the intermediary role makes recall structurally costly.

Outcome Measurement, Not Input Compliance

Frameworks that define compliance in terms of prohibited inputs (what you don’t do) are far more vulnerable to capture than frameworks that define compliance in terms of outcomes (what the land, community, or ecological system produces). Input compliance can be achieved at any scale by any actor. Outcome measurement, especially when outcomes are place-specific and community-defined, resists commodification because the measurement itself cannot be standardized away from the place.

Translation Documents, Not Compliance Documents

When engaging international standards bodies, the correct document to bring is a translation document — one that shows where the community framework maps onto international standards where overlap exists, and where it intentionally diverges and why. A compliance document accepts the international standard as the reference point. A translation document asserts the community framework as the reference point. That assertion, made precisely and early, is the difference between engaging the standard and being absorbed by it.

Name the Capture Cycle Explicitly

The most effective protection against capture is the ability to name what is happening in real time, at the working group table, before the cumulative effect of small compromises has become irreversible. This requires that community representatives in standards processes are briefed on the capture cycle — that they know Phase 2 when they are in it, and can say so. Institutional actors are not accustomed to having the process named. Naming it changes the power dynamic.

An Intemerate Note

The institution does not need to be malicious. It only needs to be itself.

Most of the people who participated in the capture of REDD+, organic certification, and fair trade believed they were doing good work. The capture was structural, not conspiratorial. The institution’s natural tendency — to standardize, to scale, to route through existing authority, to measure what is already measurable — is sufficient to hollow out a transformative framework without any actor intending that outcome.

This is why the protective architecture described above must be built into the framework’s governance before institutional engagement begins. Once the institution is in the room, its gravitational pull is already operating. The question is whether the framework has enough structural mass to maintain its own orbit.

The Intemerate Accounting advantage is that it is being designed with this knowledge in advance. That is not a small thing. Most frameworks that were captured did not see it coming. I’m laying this on the table for us to consider the parameters.