Inside Chapter 18, Trade and Sustainable Development of the EU-Mercosur?

Not Vampire, not Zombie, but Jiangshi

In the multipolar daylight, Europe is neither vampire nor zombie. The better image is the jiangshi. In Chinese folklore, the jiangshi is an old corpse that cannot generate life from within and survives by consuming the qi, the life-force of the living. That is an appropriate depiction of a fictional EU-BRICS arrangement. The issue is not whether the EU will join BRICS, it will not and to be clear it has not stated that. The issue is whether the EU can enter BRICS-adjacent growth zones and redirect that life force through European legal and regulatory systems. That is why co-option is the right term. Cooperation implies a shared design, like the Marshall Plan or the Washington Consensus. Co-option means entry, capture, and rerouting.

BRICS, as members of the G20, sits at a key intersection between OECD-linked capital and G77 development priorities. While that overlap is shifting the economic compass toward multipolar centers across Africa, Asia, and Latin America, the Global North still has advantages vis the US military expansion, as well as the EU rule making authority in Brussels. In that setting, the EU does not need formal BRICS membership to weaken BRICS autonomy. It can work through bilateral agreements, standards regimes, conformity requirements, compliance audits, and market-access conditions that can capture economic and financial growth through legal back door compliance programs.

Subscribe to Decolonize Accounting. This is a reader-supported publication. Paid subscribers will receive access to reliable and verifiable “black” papers, as well as my updated Density Debt Index

EU Environmental Harmonization

While it seems clear that Trump’s impetuous unreliability and tariff policies accelerated Europe’s move towards a more independent trade autonomy, the EU shift, with partial UK alignment, is taking advantage of its role as a major rule-exporter in digital and environmental data governance. That is why EU-India and EU-Mercosur matter beyond tariffs: they are legal channels for setting compliance in markets central to the next phase of multipolar trade.

This next phase, however, appears to be harmonizing with the 2030 timeline of the Sustainable Development Goals, and while this sounds like a positive planetary win, I would caution that from the perspective of natural capital valuation, the alignment between the SDGs, the 2025 revision of the System of National Accounts, and the inclusion of the SEEA, System of Environmental Economic Accounting, will be locking partners into external standards, verification systems, and dispute architectures controlled by Brussels. The most strategic layer is environmental data.

If SDG-era data control is now primary terrain, then much of the EU’s trade diplomacy will downstream data governance. The EU model ties access to data production, data format, traceability, and third-party verification under EU-compatible service oriented templates, likely to induce significant costs to communities, creating further barriers to access for impacted communities. EUDR traceability and geolocation requirements show this directly. INSPIRE-style interoperability shows the deeper structure: define valid environmental knowledge, then define valid market participation. In the economics of this system, cooperation is the language while jurisdiction over data is the reality.

EU-Mercosur

Chapter 18, the Trade and Sustainable Development (TSD) chapter of the EU-Mercosur agreements is framed as cooperative, but it centralizes environmental-data in EU-compatible systems: its scope links trade and investment to SDGs, entirety of Multilateral Environmental Agreements (MEAs), climate, biodiversity, forests, fisheries, and transparency, which makes environmental information a core trade object rather than a side issue (Chapter 18, scope provisions); Article 18.10 then anchors measures in recognized scientific and technical bodies and international standards, with precaution under uncertainty, which in practice advantages actors with stronger certification and interoperability infrastructures (Chapter 18, Art. 18.10); the forests, biodiversity, fisheries, and responsible supply-chain sections deepen traceability and verification expectations so market access increasingly depends on EU-legible proof of origin, legality, and sustainability (Chapter 18, thematic sections); and as stipulated in (18.15), is subject to the same dispute settlement mechanisms (21.3).

The result is the further and ongoing exclusion of indigenous, peasant, conflict displaced and climate vulnerable at-risk communities in regions already impacted by climate change and social instability. Unlike the harsh colonial methods of the 19th century or the neocolonial post war resource grabs, this is a 21st century soft-hard governance system where cooperation is the language, but one where there is a US$100 trillion+ data-validity jurisdiction that remains external to partners. Although I discuss this elsewhere, the Natural Capital valuation is one that will primarily benefit the OECD countries with the highest debt, managed by the biggest asset managers. This is neither fair nor equitable.

EU-India

The EU-India Trade and Sustainable Development chapter (Chapter 21) is comparable to EU-Mercosur on the environmental-data front, even if the chapter numbering differs. Unlike the Mercosur text, I have only seen the India draft and the technical certification aspects seem like a work in progress, without the formal institutionalized governance of Mercosur. However, the India text does combine market access with sustainability obligations that require measurable, verifiable compliance. The practical hegemony channel is external to tariff tables: exporters must increasingly produce EU-legible evidence on emissions, traceability, and due diligence to preserve access. That pressure is reinforced by EU-side regulations such as the Carbon Border Adjustment Mechanism (CBAM) and the EU’s Regulation of Deforestation-free Products (EUDR), which sit outside the FTA text but materially condition participation in the EU market. So while these market mandates may seem benign and even worthwhile, structurally, they are housed within the same structural discourse as sanctionable and hegemonic.

Both these agreements function as legal corridors where “cooperation” language coexists with EU-centered data validity, verification standards, and compliance sequencing. This all goes to show how intermediaries like auditing, validation, banking, insurance, all the regulatory administrations go towards creating value over environmental data will do little more than perpetuate the rentier economy, when alternatives benefitting planet and people could easily exist.

This is why I argue that environmental data hegemony may matter more than tariff schedules and to call the EU-India agreement the “mother of all trade deals” is more of a PR pitch. This deal will formally captured trillions of dollars of SDG data that India will produce, rather than the mere billions of dollars from market access. In this scenario it is the EU that defines the environmental data standards whose intermediaries will decide who is legible, who is fundable, and who is excluded. That is co-option, more than a blood sucking vampire, the EU is a soul snatching jiangshi, feasting on the life-source of planetary data.

BRICS and the RCEP

From this angle, BRICS and RCEP are central, not peripheral. When one considers that BRICS also lead the G77 developing countries, the Global South is expansive reaching across environmental swaths of vast forest and ocean data that should be owned and managed by the indigenous or customary stewards of these regions. Developing countries and peoples are central to the traditional rules of trade, even if they have not been central to the National Accounting revisions or the advancement of the SEEA Central Framework. And while BRICS may be building alternatives in settlement and development finance, and the RCEP in market and production integration, these institutions have not participated in the changes being made to environmental rule making in the system of national accounts. Can BRICS or the RCEP protect indigenous policy space while avoiding capture by the EU compliance systems. Can they coordinate standards that support local data sovereignty or support the development of intermediary markets that do not treat the environment as commodities to be managed by Wall Street asset management firms like BlackRock, Vanguard, or Fidelity?

So the conclusion is direct. We are moving from a WTO-unipolar legal center to a contested multi-node order. The EU is unlikely to join BRICS, but it will continue trying to shape BRICS-adjacent trajectories through legal insertion and standards power. The US remains constrained by a debt-military nexus that relies on coercive trade tools and security pressure to try to extend their influence.

The emerging center across BRICS and RCEP, with strong China-ASEAN weight, can hold if it avoids two traps. The first is vampire economics: neoliberal privatization that extracts public capacity. The second is zombie stabilization: permanent emergency financed by debt and militarization. If multipolar institutions reproduce either trap, the old crisis returns like a spirit snatching jiangshi.

Future casting

If BRICS can support initiatives taking place within the G77 when it comes to local data sovereignty, and the establishment of alternative valuation schemes that can benefit trans local intermediary markets within BRICS new payment, finance, and trade systems that will protect social reproduction and sovereign development space, then the transition can endure. The strategic task is to keep qi in living societies and out of exhausted empires, even when co-option arrives politely, over tea and weiqi.

Key references

System of National Accounts (2025) SDG Report (2025) SEEA Central Framework (2012) SEEA SEEA Natural Capital Accounting For Integrated Biodiversity Policies (2020) World Bank Changing Wealth of Nations (2018) European Commission EU-India Agreements (2025) European Commission EU-Mercosur Agreements (2026) European Commission-INSPIRE Knowledge Base European Commission-Regulation of Deforestation-free Products European Commission-Carbon Border Adjustment Mechanism BRICS https://infobrics.org/ RCEP Regional Comprehensive Economic Partnership

This is a call for Marxists to begin to treat accounting as more than a technocratic background. I would argue that the most powerful battlefield of economic governance is in the field of accounting and its intermediaries. A 21st-century Marxist approach has to include accounting.

For those who have been following our call for stronger civil society engagement in the revision of the UN System of National Accounts, including critiques of the SEEA and the SDG framework, this is the argument.

National accounting may look technical and administrative, yet it is foundational. It determines what an economy is allowed to “see,” what states are expected to optimize, and what becomes eligible for finance, compliance, and enforcement. It shapes how inequality is recorded, how labor is recognized or erased, and how environmental harm is treated as costless background. Changing accounting rules changes the structure of value itself. That is one of the most direct ways to challenge global capitalism’s operating system.

If Marx were writing today, he would likely treat data as a primary site of labor, ownership, and class power.

This piece is anchored in a concrete institutional shift that is already underway. In March 2025, the UN Statistical Commission adopted the 2025 System of National Accounts as the new global standard, with an expanded focus on well-being and sustainability. The 2025 SNA is not a side debate. It is the template that shapes what governments measure, what they report, and what becomes legible to trade rules, climate finance, insurance pricing, procurement, and macroeconomic surveillance. Once sustainability and environmental reporting become embedded in the core statistical standard, the struggle moves from policy rhetoric to accounting definitions and enforcement routines.

The environmental dimension is being formalized through closer alignment with the UN System of Environmental-Economic Accounting. The SEEA Ecosystem Accounting framework was adopted by the UN Statistical Commission in 2021, and the SEEA Central Framework is now treated as a major macroeconomic statistical standard that complements the SNA. This matters because it is how ecosystems, resources, and “sustainability” become governable inside national balance sheets and national aggregates. The accounting system decides what counts as an asset, what counts as depletion, what counts as value, and what counts as an externality. Those decisions shape who gets paid, who gets regulated, and who is disciplined.

That is why decolonizing accounting is not a slogan. It is a demand for measurement sovereignty. If the 2025 SNA and SEEA-linked implementation is operationalized through, for example, the Sustainable Development Goals, through the existing architecture of standards, audit firms, ratings agencies, and asset managers, ecosystems and development will be treated as balance-sheet inputs and communities will be treated as data suppliers. This recreates colonial extraction through measurement, where the Global South becomes another table of compliance while the North captures rents through proprietary models, centralized clearing, and securitized “green” products. The same capture logic can travel through top-down carbon markets, debt-coded loss-and-damage delivery, reinsurance and parametric triggers, and tokenized “green” financial instruments, even when they are branded as climate solutions.

The alternative pathway is to treat environmental data as data labor, collective property, and collective wealth. Communities generate high-value information through stewardship, daily survival, exposure to risk, and restoration work. That data belongs under community governance, with Free, Prior, and Informed Consent and enforceable limits on reuse. If communities control baselines, verification, and licensing, they can build translocal, interoperable data markets that fund restoration and livelihood security rather than feeding financial capture. Multipolarity matters here because it increases the number of institutional routes for exchange and settlement, which makes it harder for a single financial center to monopolize standards, pricing, and enforcement.

Receive benefits for subscribing to Decolonize Accounting. Every paid subscription helps.

Workers of the data world, unite. You have nothing to lose but your block chains.

The closing line of The Communist Manifesto, “Workers of the world, unite. You have nothing to lose but your chains.”(1848), frames environmental measurement as a labor relation, where communities produce value through lived conditions and stewardship while others capture the surplus.

National accounting is moving toward environmental economics and expanded environmental reporting. If that shift arrives through the existing institutions of finance and standard-setting, it will treat ecosystems as balance-sheet inputs and it will treat communities as data sources. That pathway reproduces colonial extraction in a new form. It takes measurement authority away from customary governance and places it inside top-down audit firms, ratings agencies, and asset managers. Decolonizing accounting is necessary because the first battle is definitional. Whoever defines the variables, baselines, and verification rules controls the market that follows.

The data owners are the ruling class of the digital age.

From The German Ideology, Part I “Feuerbach” (1947). “The class which has the means of material production at its disposal, has control at the same time over the means of mental production …” (p.59). Referencing the simple rule of power: whoever owns data infrastructure and standards sets the terms of trade, compliance, and credibility.

We already live in a bifurcated economy. One segment lives inside asset inflation, stock indices, and paper wealth. The other lives inside wages, rents, food prices, energy bills, caregiving, and environmental insecurity. If environmental economics becomes another investable layer owned and managed from the top of that asset world, the bifurcation deepens. Communities will be forced to disclose ecological and social conditions for compliance, while outside institutions capture the revenue through intermediated finance, proprietary models, and securitized products.

Data is a thing. Environmental data is the means of reproduction.

From Capital, Vol. 1, Part III, Chapter VII “The Labour-Process …” (1967). The classic construction of Marx’s “An instrument of labor is a thing, or a complex of things…”) (p.179). The paragraph goes on to describe how “the earth is an instrument of labor, but when used as such in agriculture implies a whole series of other instruments and comparatively high development of labor.”

This matters because environmental reporting is becoming a gatekeeper for credit, insurance, procurement, and cross-border market access.

A different outcome is possible if environmental data is treated as labor, property, and collective wealth. Communities generate high-value information through stewardship, daily practices, risk exposure, and restoration work. That data should remain under community governance through Free, Prior, and Informed Consent, local protocols, and enforceable rules on reuse. Under an Intemerate Accounting approach, the goal is to fund restoration and social resilience as measurable work, verified locally, and exchanged through markets that remain multipolar and translocal.

All that is measured becomes tradable. All that is unmeasured becomes disposable

From the opening line of Capital, Vol. 1, Part 1, Chapter 1 “Commodities” (1967), Marx writes “The wealth of those societies in which the capitalist mode of production prevails, presents itself as a “an immense accumulation of commodities…” (p35). This is the political risk of environmental economics as it is currently being designed, because who accumulates the measurement determines who receives funding and who becomes invisible.

Cap-and-trade and carbon markets show how “climate compliance” can become a market for paper instruments that preserves environmental harm while purchasing credits elsewhere, while offset projects can also trigger land and rights conflicts when communities are treated as project sites rather than governing authorities.

To keep this market from being absorbed by Wall Street, the design has to block the usual capture routes: exclusive ownership of standards, central clearing controlled by large financial firms, leverage through debt instruments, and securitization that turns community obligations into tradable claims. The market needs distributed governance, community-controlled verification, non-extractive licensing, and limits that prevent data rights from becoming collateral. It also needs multiple interoperable nodes across regions, so no single financial center can set the price, the model, and the enforcement terms.

The ideas of the ruling class are the data of the ruling class

In the construction of his history of consciousness in The German Ideology, Part 1, Feuerbach (1939), the original text is , “The ideas of the ruling class are in every epoch the ruling ideas…” (Marx & Engles, 1939, p 89).

This should clarify why decolonizing accounting starts with categories and definitions, since historical categories decide what counts as “nature,” “risk,” and “value,” as we update them from the 19th century to the data infused 21st century.

When standards are written far from the places being measured, they convert customary relationships into external variables. They also embed assumptions about property, productivity, and legitimacy. The result is a quiet transfer of authority from communities to institutions that can certify, rate, and monetize the measurements.

Loss-and-damage finance, for example, can be undermined when delivery is mediated through institutional hosting arrangements and loan-heavy funding models that deepen debt burdens and constrain public budgets, which shifts repair into a creditor relationship instead of an obligation rooted in responsibility.

Accumulation of data wealth at one pole means accumulation of data poverty at the other.

From Capital, Vol. 1, Part VII, Chapter XXV “The General Law of Capitalist Accumulation,” Marx describes how the “Accumulation of wealth at one pole is … at the same time accumulation of misery …” (p.645). This is the predictable outcome when communities are exploited by a despotism more hateful for its meanness. The image of “law riveting the labourer to capital more firmly than the wedges of Vulcan did Prometheus to the rock,” should remind us, that at this moment, where there is a paradigm shift in the accounting matrix, there is a brief window of opportunity, to finally overturn the very system that binds us to the rock.

Environmental disclosure without local ownership produces one-way transparency. Communities supply information and absorb enforcement pressure, while external actors hold the models, the platforms, the legal rights, and the revenue. Data poverty shows up as forced disclosure, weak bargaining power, and no remedy when data is reused against community interests.

Reinsurance and parametric “rapid payout” schemes can also replicate this imbalance through basis risk and model-driven triggers, where investors and insurers price the instrument while communities, taxpayers, and governments carry the consequences when payouts miss lived losses.

Expropriate the data-expropriators, or the integument is burst asunder

From Capital, Vol. 1, Part VIII, Chapter XXXII “Historical Tendency of Capitalist Accumulation,” when Marx writes “the expropriators are expropriated,” he is projecting how the logic of accumulation will conclude (p.763). “One capitalist always kills many, and in the narrowing centralization of ownership and accumulation, “the integument is burst asunder.” (haha, meaning that capitalist centralization eventually ruptures under its own contradictions.)

This is a governance statement about reversing extraction, where communities reclaim control over the measurement system and the income streams built on top of it.

The practical requirement is not isolation from markets. The requirement is market structure that prevents permanent alienation of data rights and blocks the consolidation of standard-setting into a small number of firms. The architecture has to keep consent, verification, and licensing enforceable at the community level.

As a warning to central planners, environmental crypto products and tokenized carbon markets can add another backdoor layer of centralized financialization, where credits are repackaged into tokens, where speculation inflates prices, and “impact” claims become detached from on-the-ground repair and consent. The reliance upon these kinds of financial products in an economy overly dominated by wealth accumulation, should only be seen as momentary salve.

From each community according to its data labor, to each community according to its ecological needs

This is central in the sense that it is tied to moral governance. In Marx’s Critique of the Gotha Programme, passage on the “higher phase” of communist society (p.10) “from each according to his ability, to each according to his needs!” which Lenin addresses in his State and Revolution, “The Higher Phase of Communist Society” (pp 81-82 in this volume).

Marx’s “higher phase” is a claim about measurement and distribution becoming social habits rather than coercive administration. It rests on a shift in the conditions of life. The division of labor stops subordinating people. Labor becomes life’s “prime want.” Cooperative wealth flows more abundantly. Only then can society leave behind the “narrow horizon of bourgeois right” and adopt the rule, “From each according to his ability, to each according to his needs.” Lenin reads the same passage as a problem of governance, since the state “withers away” when people no longer require an external authority to police distribution and when productive capacity and social habits make voluntary contribution and free access workable.

In this context, an ecological based decolonial accounting frame translates that argument into the present conflict over environmental measurement. Environmental accounting will increasingly decide the flow of finance, adaptation support, and restoration investment. The question is whether those flows are governed by external standards and investor logics, or the interactions, or by protocols of reciprocity set by the communities who bear the risks and do the work. The “higher phase” in this register is not a slogan about abundance alone. It is an institutional condition in which distribution follows collectively governed protocols, and measurement is owned by those who generate the underlying reality.

That begins with a different definition of production. Under contemporary environmental economics, value is often assigned to “assets” and “services” abstracted from customary relations. Under decolonial accounting, the primary productive act is stewardship and restoration, including theinteraction that documents conditions, validates change, and carries consent. Measurement becomes a community right and a community obligation. It becomes a protocol: how baselines are set, how evidence is gathered, who can verify, what can be shared, what must remain protected, and what reciprocity is required when outsiders benefit. This is the point where Marx’s line about “bourgeois right” becomes practical. Bourgeois measurement insists on commensuration, exchange equivalence, and external audit authority. Decolonial measurement insists on consent, context, and remedy.

From a translocal and FPIC perspective, communities do not need one universal metric designed in distant institutions. They need interoperable pluralism. Protocol becomes the shared engagement that allows different communities to coordinate exchange while preserving local authority. In practice, this means data can travel across regions and institutions only through terms that carry the source community’s governance, including revocation, use limits, and benefit shares. Interoperability serves reciprocity rather than extraction. The market follows the protocol, rather than rewriting the protocol to fit the market.

Distribution then stops being a downstream “allocation problem” and becomes a design principle. Marx’s higher phase shifts the unit of concern from equalized exchange to needs-based access. In decolonial environmental accounting, this means restoration finance and adaptation resources should not be allocated mainly by bankability, creditworthiness, or investor return targets. They should move according to ecological harm, vulnerability, and the labor required for repair. Communities contribute according to their capacities and situated knowledge. Communities receive according to the ecological and social needs produced by histories of dispossession, exposure, and underinvestment. That is the core redistributional meaning of “from each…to each…” once measurement is treated as a political economy question instead of a technical one.

A “higher phase” outcome becomes plausible when three things converge. Measurement authority sits with communities through protocol and reciprocity. Verification is locally rooted and translocally legible. Distribution is governed by needs and repair, rather than by external equivalence rules that treat every community as a comparable unit in an investor portfolio. Marx’s banner line is then no longer only a moral horizon. It becomes a governance claim about who decides the flows of markets, because accounting decides what is real, what is owed, and what can be enforced.

The price-form hides the data-form. The metric looks neutral while power moves through it

From Capital, Vol. 1, Part I, Chapter III “Money, or the Circulation of Commodities” , Marx discusses the price/money-form. To quote:

“The price or money-form of commodities is, like their form of value generally, a form quite distinct from their a palpable bodily form: it is, therefore, a purely ideal metal form. Although invisible, the value of iron, linen, and corn has actual existence in these very articles: it is ideally made perceptible by their equality with gold, a relation that, so to say, exists only in their own heads. Their owner must, therefore lend them his tongue, or hang a ticket on them, before the prices can be communicated to the outside world (p.95).

To understand why it is important to resurrect Marx in the 21st century, we need to consider where money and monetary value sits inside the data form:

Ecological realities have palpable forms. A river has flow and contamination. A forest has biomass and species relations. A community has health burdens, food security, and exposure to storms. None of these speak in a market language on their own. To make them tradable, they must be converted into a measurement form that can circulate. That conversion is the ecological equivalent of the price tag. It is metadata, indicators, baselines, scoring rules, verification protocols, and reporting templates.

The “ideal form” in the data economy is the metric. A biodiversity score, a carbon ton, a resilience index, or a risk rating is not the ecosystem itself. It is a standardized statement that claims equivalence across places and lives. It can exist as a number in a database long before it corresponds to any lived improvement on the ground. Once expressed, it can be bought, sold, insured, securitized, or used to approve or deny funding. That is why metrics have power. They convert complex life into an exchangeable unit.

The “owner lends them his tongue” becomes a question of who has the authority to speak for the ecosystem. In top-down environmental accounting, the tongue belongs to institutions that set standards and certify claims: auditors, ratings agencies, large NGOs, consultancies, and financial platforms. They decide what counts as a “forest,” what counts as “degradation,” what counts as “restoration,” what time horizon matters, what uncertainty is acceptable, and what proof is required. Communities then become suppliers of raw observations, while outside actors control the language that turns those observations into financial instruments and compliance categories.

Decolonial accounting targets that exact choke point. It says communities must own the measurement tongue. They must define baselines and categories through customary governance and Free, Prior, and Informed Consent. They must control how ecological data is collected, stored, verified, and licensed. They must also control the right to refuse, the right to revoke, and the right to demand reciprocity. In this frame, ecological data is data labor and collective wealth. The metric is not allowed to detach from protocol. The price tag cannot be hung on a community’s environment by someone else.

This is also why capture risk is predictable. Once ecological data is turned into standardized metrics, it becomes easy to route value upward through familiar mechanisms: proprietary scoring models, centralized registries, pay-to-play certification, and securitized “green” products. A decolonial approach breaks that chain by insisting that the measure is not just a number. It is a governed relationship. The metric must carry the community’s terms of use and benefit, so the market cannot treat the ecosystem as a silent object and treat people as a passive dataset.

The Intemerate Equation

This is where the intemerate equation comes in. It is a tangible equation that can be used to produce metric data. Data is acquired through a community defined baseline across time. It establishes a baseline expectation according to what communities define. It measures the deviations, tracking the trajectory on a timeline. By itself, these might just seem like inconsequential numbers that have no bearing on values that can be interpreted monetarily, but this is where intermediary markets come in. They are the core facilities for scoring data values into monetary values.

Intermediary Markets

Intermediary markets can sit between local data sovereignty and interglobal exchange, while keeping authority close to the people who bear the ecological and economic risks. Community data cooperatives and trusts can hold environmental datasets, set consent terms, and negotiate licenses as a collective. Local verification and audit guilds can validate baselines, methods, and outcomes, with indigenous and customary authority embedded in the audit standard. A restoration procurement market can pay for verified actions and services, including monitoring, remediation, regenerative agriculture, watershed work, and biodiversity recovery. A compliance translation market can convert local indicators into reporting formats required by governments or cross-border standards without surrendering underlying ownership. A data licensing exchange can grant time-bound, purpose-bound access rights, priced for use and reciprocity, with community veto and revocation built in. A reciprocal benefit and dividend market can route a defined share of any downstream value back to the communities that generated the data and did the work. A risk mutual and insurance market can use community metrics to price adaptation support and disaster recovery without predatory premiums or exclusionary rules. A dispute resolution and remedy market can provide arbitration, enforcement, and sanctions for misuse, including penalties for unauthorized reuse and mechanisms for restitution.

The point of these intermediaries is functional power. They translate data sovereignty into real exchange without surrendering the means of measurement. That is how multipolar, translocal, interglobal markets can grow without becoming another extractive frontier. When communities own the baselines, the verification ledgers, and the licensing terms, environmental economics can fund restoration and livelihood security on community-defined conditions. If they do not, environmental economics becomes an external management regime where Global South, displaced, and marginalized communities supply the metrics while Wall Street and allied intermediaries capture the rents.

Data clicks/cliques

In the older party-state usage, “cliques” usually meant organized factional loyalty networks inside a centralized organization, seen as competing with formalized state discipline and sometimes treated as a threat. In a data context, “data clicks/cliques” can describe decentralized, implied agreements among people and communities who share norms, methods, and obligations across distance. They are less about capturing a single hierarchy and more about building distributed trust.

In practical terms, a translocal data clique is informal and may share a in a particular market . Members adopt shared protocol for consent, verification, reciprocity, and enforcement. They recognize each other’s audits. They share templates and methods. They coordinate refusal when terms are extractive. They also coordinate exchange when terms are fair. This makes a market possible without surrendering measurement authority to one central registry or one financial hub.

The danger is that cliques can still become gatekeepers. They can become exclusionary, opaque, or captured by charismatic brokers. The safeguard is to keep clique power conditional and when those conditions hold, “data cliques” become a decentralized infrastructure for decolonial accounting rather than a backdoor hierarchy.

References

Marx, Karl, and Friedrich Engels. Ten Classics of Marxism. The Communist Manifesto. 1940 International Publishers, 1947. Marx, Karl. Capital: A Critique of Political Economy. Vol. 1, International Publishers, 1967. Marx, Karl, and Friedrich Engels. Edited. by R. Pascal. The German Ideology. Parts I & III. International Publishers, 1939. Marx, Karl. Critique of the Gotha Programme. International Publishers, 1938. Marx, Karl. Grundrisse. The Pelican Marx Library, 1973 Saiki, Arnie. Ecological-Economic Accounts: Towards Intemerate Values. Pacific Theological College, 2020. Saiki, Arnie. Intemerate Earth. “Posts”, https://intemerate.earth/blog. Accessed 29 Jan. 2026.

The IF20 Religion and Environment Working Group’s 2025 policy brief frames the debt–climate nexus as an existential constraint on low-resource countries, where debt servicing displaces public services and climate response. Building from a proposed UN-centered debt framework, this article focuses on precautionary dangers inside SDG or national accounting instruments, since swaps and valuation-based relief can become predatory when they shift territorial and resource decision-making through external monitoring and data custody. FPIC and locally held data sovereignty through community banking custody must be treated as environmental security measures for the Global South before any new market architecture is allowed to form.

FPIC First: Environmental data is a security issue.

Free, Prior, and Informed Consent has to sit at the front of any environmental data regime that feeds national accounting and climate debt relief. FPIC is a jurisdictional safeguard protecting Indigenous and local authority over knowledge, measurement, and the downstream uses of that measurement in law, finance, and policy.

At this point, environmental data should be treated as strategic infrastructure. For much of the Global South, and especially, Indigenous Peoples, poor, peasant, displaced, and climate or conflict vulnerable at-risk communities, environmental data is a security issue. The UN system has adopted standards that make ecosystem accounts more legible to states, lenders, and markets. The United Nations Statistical Commission adopted the SEEA Ecosystem Accounting standard in March 2021. The United Nations Statistical Commission adopted the System of National Accounts 2025 as the updated international standard for national accounts. These changes matter because they widen the space for monetary valuation of ecosystems and natural resources inside recognized accounting frameworks. OECD guidance for implementing SNA 2025 explicitly frames “natural capital” as the aggregation of natural resources and ecosystem assets and discusses how depletion and related treatments shift net aggregates and policy.

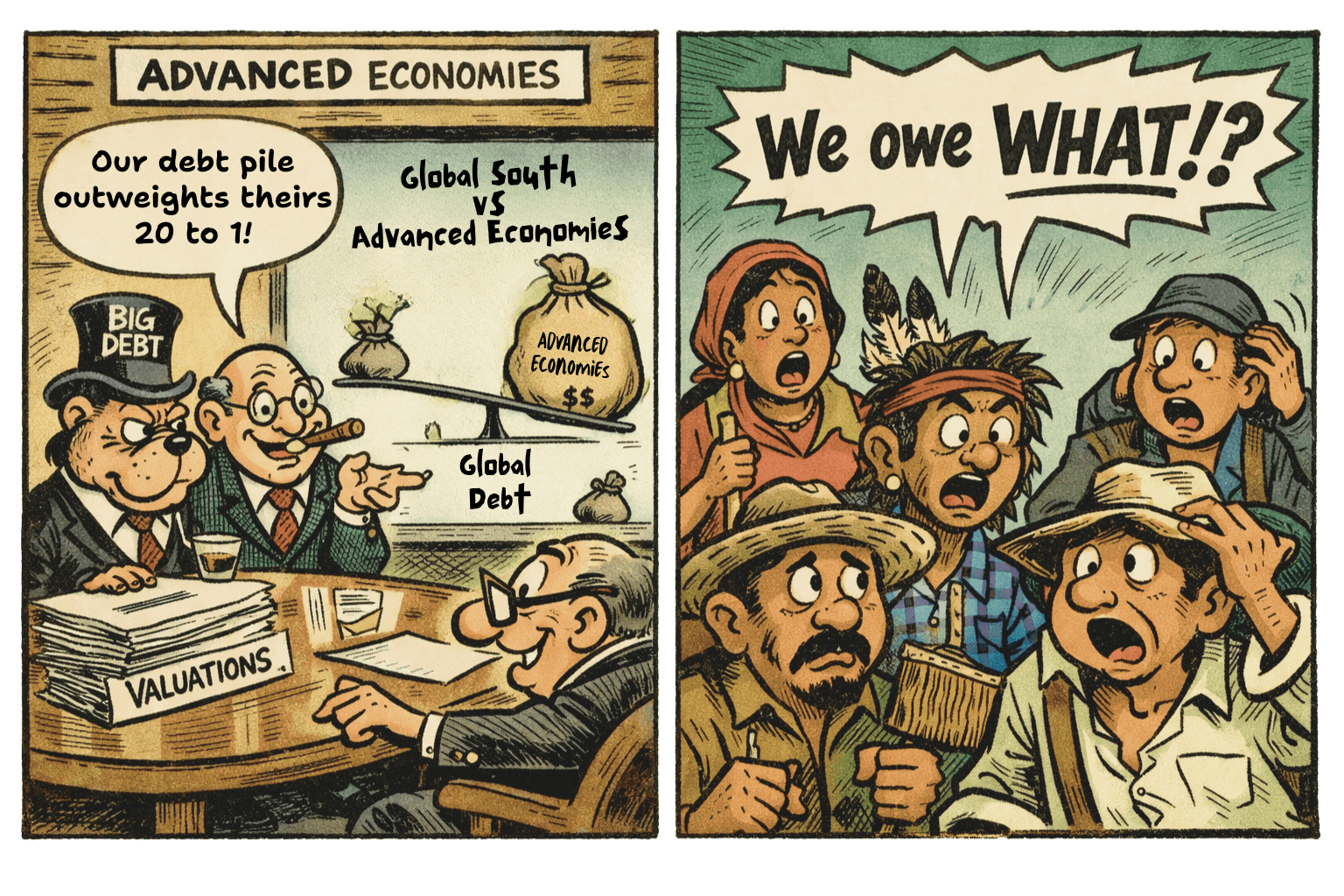

To be absolutely clear, debt distress is the condition that makes this accounting shift politically dangerous. Global public debt is now near the US$100 trillion mark, and total global debt (public and private) is above US$250 trillion. UNCTAD documents a widening crisis in which a rising number of countries spend more on interest than on basic services and highlights the scale of public debt and servicing constraints. For the poorest and most climate-vulnerable countries, IIED reports debt repayments roughly double the climate finance they receive, which clarifies the fiscal trap that drives governments toward fast debt deals.

This is where “back door” strategies enter. We should not be surprised if the pictures of smiling children depicting friendly, trustworthy care is a Wall street wolf in disguise. These wolves might wear keffiyehs to look like relief. They may come wearing slippers and a climate march hoodie to discuss risk reduction. They might wear hard hats to inspire technical assistance. They might carry a tote bag to convey conservation. But they are all suits and these remain contractual top-down mechanisms. A country accepts a restructuring instrument that ties debt relief to environmental performance, monitoring, and governance conditions. Those conditions can outlast administrations and can shift real authority over land-use decisions, customary livelihoods, and data systems away from communities and toward external stakeholders.

Debt-for-nature swaps show the pathway. These swaps refinance or repurchase debt and link the fiscal savings to $100 billion conservation commitments overseen through dedicated governance vehicles and monitoring arrangements. Even when the conservation goals are sound, the governance questions remain. Reuters reporting on Ecuador’s Galápagos swap describes complaints from local groups alleging inadequate community engagement and transparency, alongside a formal review by the Inter-American Development Bank’s accountability mechanism. That dispute is not arbitrary and has been one of the core issues propelling the 2020 Intermerate Manifesto. It is the core risk. When environmental value becomes part of a debt contract, communities can be treated as an implementation detail rather than rights-bearing authorities.

FPIC is a safeguard addressing that risk because it governs the full lifecycle of data and valuation. UNDRIP requires states to consult and cooperate in good faith through Indigenous representative institutions in order to obtain FPIC for measures that may affect them, and it sets FPIC expectations around projects affecting lands, territories, and resources. ILO Convention 169 sets binding consultation requirements for ratifying states, including consultation through appropriate procedures and representative institutions regarding legislative or administrative measures that may affect Indigenous peoples directly. Together, these instruments frame FPIC as a governance threshold that cannot be waived in moments of fiscal distress.

However, it is necessary to add, that what is binding is only as good as what is enforceable, and the recent spate of impunity occurring amidst the grossest crimes against humanity, provides little confidence or what international law means when it comes to genocide or safeguarding against ecocide, as with U.S. unilateralism concerning deep seabed mining, or even the impunity of ICE agents, ignoring the constitutional rights of its citizenry.

An accounting shift will create new intermediary markets. That outcome is structural and predictable. Once states publish ecosystem accounts and embed them in planning and financing, there will be demand for baselines, monitoring, verification, and performance claims. Those claims will be organized into instruments that pay for restoration, watershed protection, biodiversity outcomes, and disaster-risk reduction. The market question is not whether claims will emerge. The market question is who controls the stack of measurements that defines the claims and who benefits from them.

If the measurement stack is controlled outside the Global South, then “natural capital” becomes just another layer of dependency. Control is exercised through proprietary models, remote sensing pipelines, audit standards, verification firms, platform custody, and dispute venues. A country can retain nominal sovereignty over territory while losing practical sovereignty over the numbers that govern policy space. SNA 2025 (chapter 35) and SEEA EA (Section D & E) adoption increases the likelihood that these numbers will be treated as official and comparable. This integration is weaponizable, and while its adoption could be a seismic reset for the global economy, considering there is literally zero discussion in the public space, and little attempt at embracing local data in local contexts or local markets, suggest that the impending reset is going to bypass those that are most in need of a reset.

Local data sovereignty needs custody. This is where practical initiatives like a community-bank becomes a serious institutional safeguard. Environmental data and stewardship data should be treated as collective assets held under fiduciary duty with explicit limits on alienation. A “community data bank” model should be literal, through community banks, credit unions, or public development-bank windows. It can also be implemented through legally chartered data trusts or cooperatives that use banking-grade custody rules and are accountable to communities and domestic public law. The function is the same. The institution holds the keys, enforces FPIC permissions, and blocks secondary uses that convert local data into external leverage.

This custody layer matters because regardless of broken contracts and agreements that might take place under FPIC, locally held data will provides communities with leverage. If communities cannot own local markets or initiatives, climate debt relief contracts can smuggle control through technical clauses.

For example, a contract can embed third-party monitoring that becomes permanent. A contract can route disputes to external arbitration that privileges investor claims. A contract can require data submission to vendor systems with derivative rights and restrictive licenses. A contract can include step-in rights that transfer implementation authority when targets are missed due to climate shocks…

As a precaution to another century of hegemony, these are not hypothetical instruments. They are common legal design patterns in contemporary finance. The difference here is that the subject is ecological governance, and the collateral logic is performed through “valuation” rather than title transfer. And to be clear, it is for us to define the value of our environment, our well being, and our bones, and if that value is sacrosanct, then that is for us to decide and to protect.

A Global South safeguard framework

Even beyond the rights of Indigenous Peoples, FPIC has to broadly apply to data collection, data storage, model design, baseline selection, verification rules, and any contract that monetizes or conditions debt relief on environmental metrics.

Environmental accounts used for national planning should be separated from monetized claims used in financial contracts. Planning accounts is public-interest infrastructure. Monetization should require an additional legal gate that includes FPIC and a domestic public-interest test. We need a multipolar framework that considers translocal or interglobal accounting, auditing, regulations, compliance, and enforcement.

Debt relief should be delinked from ecological collateralization. Debt restructuring is existential, yet it should not be purchased by converting ecosystems into long-run performance liens. UNCTAD’s debt diagnostics already show that servicing burdens are displacing basic services and development capacity (UNCTAD xx). Relief needs rules-based debt workouts and grant-based climate finance, with environmental accounting used to plan restoration and to document harms and reparative claims, rather than to securitize nature.

The G20 is the right venue to discuss this. We are in a shifting balance of power between the OECD and the BRICS economies, the multipolarity of BRICS+, is better leveraged to write new rules for the global economy and support the kinds of local data sovereign networks, for the future. BRICS+ are poised to defend against the Network State, and against a tyranny of Assets under Management.

Finally, Global South countries need compilation and verification capacity that prevents vendor dependence. The point is not to reject international standards. The point is to prevent international standards from becoming a channel through which external actors capture domestic policy. SNA 2025 and SEEA EA will be implemented unevenly. While they are within the United Nations, they are largely dominated by OECD members and policy directors.

Debt relief and environmental accounting can support poverty reduction and restoration. That outcome requires governance architecture. FPIC is the front gate; community data custody is the lock; and South-led standards implementation is the long-term defense.

_____

Disclosure: The writer is a member of the G20 Interfaith Forum (IF20) Environment Working Group. The views expressed in this article are his own and do not represent the positions of the Environment Working Group, the IF20, or any other IF20 participants.

Citations

International Monetary Fund. “Global Debt Remains Above 235% of World GDP.” IMF Blog, 17 Sept. 2025.

International Institute for Environment and Development. “World’s least developed countries spend twice as much servicing debts as they receive in climate finance.” IIED, 16 Oct. 2024.

International Labour Organization. “Indigenous and Tribal Peoples Convention, 1989 (No. 169).” OHCHR treaty text portal.

OECD. “Measuring Natural Resources in the National Accounts.” OECD Publishing, 18 Dec. 2025.

Office of the United Nations High Commissioner for Human Rights. “Consultation and free, prior and informed consent (FPIC).” OHCHR.

Reuters. “Debt-for-nature swaps could give $100 billion boost to climate fight, says report.” 15 Apr. 2024.

Saiki, Arnie. Ecological Economic Accounts: Towards Intemerate Values. Pacific Conference of Churches, Pacific Theological College, University of South Pacific, 2020.

UN Trade and Development. “A World of Debt 2025.” UNCTAD, 2025.

United Nations. “United Nations Declaration on the Rights of Indigenous Peoples.” UN, 2007.

United Nations Statistics Division. “System of National Accounts 2025.” UNStats, 2025.

United Nations System of Environmental-Economic Accounting. “Ecosystem Accounting.” UN SEEA, 2021.

My meandering conversation with Professor “Marina” about the auditing framework.

I had lunch yesterday talking to Professor “Marina” who teaches accounting at PCC. We were at a cafe in Pasadena.

Decolonize Accounting is a reader-supported publication. To receive new posts and support my work, consider buying my lunch like Marina did.

Marina: So, Arnie, I get that you are excited about these indigenous-led auditing frameworks and “intemerate accounting,” but I have a basic question. How can protocol, reciprocity, even something like the “valuation of bones,” ever be as reliable as standard Western accounting? I trust GAAP, IFRS, SEC filings (see annex). I do not see how protocol and trust networks can replace that.

Arnie: They do not replace it. They redefine what is material and who gets to verify it. Western accounting starts from the firm and the state. Intemerate accounting starts from the community and their traditional home. The question is not whether protocol or reciprocity substitutes for evidence. The question is what counts as evidence and who is allowed to produce and audit it.

Marina: But reliability depends on standardized rules, independent auditors, and transparency. Markets trust that. Communities are important, but that sounds subjective. How do you prevent capture or favoritism if the auditors are “from the community”?

Arnie: Start with the structure. An intemerate audit has several layers. There are community-defined protocols. These are the rules that say who speaks for land, water, graves, fishing grounds, and so on. They already exist as customary authority. There are also ecological and social baselines. These are measured conditions: fish counts, soil health, water quality, food security, displacement risks, and cultural sites. Then of course, we have the intemerate auditor trained in ecological resilience. This person learns statistics, accounting, and local protocol. Their job is to document those baselines and track changes. Also, there are external peer reviews by other indigenous or community-based auditors, or local governments, science communities, international organizations… people who are not from that village or that project. We’re dealing with comparative data, and if local data sovereignty can really be a thing, we would need someone who can verify data while prioritizing community consent.

Arnie: You get reliability because no single actor controls the data. Local knowledge sets the categories. Technical training standardizes the methods. Peer auditors check the work.

Marina: You are describing a profession, almost like a CPA, but for ecology and culture. What makes that different from an ESG consultant?

Arnie: In intemerate accounting, the community owns the raw data. Auditors and intermediaries only get “licensed” access. That reverses the usual ESG arrangement where consultants extract data for investors. ESG is designed to protect investor portfolios. Intemerate accounting is designed to protect community resilience and ecological restoration. Investors can still participate, but they have to adjust to community-defined baselines, not the other way around.

Marina: Let me push back. I am all for indigenous rights. But when you talk about “bones” and “ancestral remains” as variables in an audit, I worry you are drifting into something really abstract. How do you “value bones” in a way that a bank, a pension fund, or even a development bank can understand?

Arnie: Start by defining what the “valuation of bones” actually means. It is never the act of pricing a skull or attaching a market figure to ancestral remains. It is the recognition that burial grounds, genealogical obligations, and ancestral sites are sacrosanct. They sit outside the field of commodification. Treating bones as something to be measured in money requires erasing a people’s history. That is the premise that underlies genocide.

Arnie: Let’s look at Tuvalu, where Australia is essentially pushing for a citizenship-for-territory swap. You couldn’t pay me enough to work on a project like that. Trading your bones for citizenship is really like a history of warfare, where the victor desecrates ancestral bones. Submergence does not dissolve the connection. The relationship to land, spirit, and lineage persists even when terrestrial life becomes difficult. Communities adapt; they create the technological capacity to make settlement functional, unless, of course, they just want to leave, but that’s different from relinquishing one’s ancestral claim.

Also, that continuity is a measure of resilience. It carries more value than any external valuation of land could provide. It is not a financial metric. It is a measure of identity, obligation, and endurance that no external accounting framework can replace.

Marina: So you are reframing “bones” as a structured constraint and a permanent liability, not as some mystical add-on. Fine. But then we still have the question of transparency. Western accounting standards are open. Anyone can read IFRS rules. I do not see that with your accounting matrix. How do I trust that these indigenous audits are not just a cover for local graft?

Arnie: Western rules are open on paper, but you know very well that a lot of the real decisions happen in private back rooms, tax rulings, and side letters. Transparency is not just about publishing standards. It is about who can see the data and contest it.

In an intemerate framework, transparency works in two directions. Horizontally, inside the community, people see how baselines and scores are produced, and of course, they can challenge them. Vertically, any external funder would get a standardized summary: resilience scores, risk flags, protocol obligations, data provenance, whatever the needs are.

Arnie: The audits show which indicators are community-verified, which are satellite-verified, which are third-party lab results, and where there is disagreement. That is often more honest than a single “impact score” in a glossy ESG report.

Marina: You know my concern. BRICS and BRI- these multi-lateral arrangements look like geopolitical tools. They talk about “win-win” and “South-South cooperation,” but the deals are negotiated behind closed doors. Debt terms can be harsh. Why would I trust an “indigenous audit” that is plugged into that ecosystem?

Arnie: You should not trust it blindly. The point is that an intemerate audit gives communities leverage in any ecosystem, whether it is BRICS, BRI, or OECD finance— it’s just that I don’t believe any country within the OECD system would engage in a system that ultimately doesn’t benefit them or allow them to set the rules of the system. We’ve already seen what the World Bank is trying to do with FPIC. How do you standardize any Indigenous Peoples’ process for Free, Prior, and Informed consent? Multilateralism within the regional context provides far more flexibility, and in my opinion, can move very quickly. Look at COP, the big countries will drag their feet until climate is past the tipping point, then they will act when they hold all the cards. I’m sorry, I don’t want to live in that world. There have to be other options… remember, another world is possible, and an alternative accounting matrix is probably the most straightforward way to get there.

Arnie: If a bank wants to fund a port or a road, the intemerate audit says: Here is the current social and ecological baseline. Here are the community’s non-negotiable constraints. Here are the obligations and revenue flows needed to improve resilience rather than degrade it. Here are the conditions under which we will share our data or revoke consent.

Arnie: That makes the deal legible and contestable. If the bank ignores the audit and the project goes bad, there is a clear record that the community flagged the risks. It becomes evidence for renegotiation.

Marina: But does any bank actually care? I work around institutional investors. They like clean numbers: internal rate of return, net present value. They would put ESG on top if they have to, and that is probably less the case now under Trump. But they do not rewire their models around local cosmologies.

Arnie and Marina: Trump… lol…omg…Epstein…(expletives and such)…

Arnie: At the end of the day, the international accounting framework has to change, so why not start from an equation that cannot be dominated by Western accounting practices? Accounting is the fundamental that locks in conditions of colonialism, and to decolonize accounting, in my opinion, that’s the most important act.

Arnie: The intemerate auditor is the person who can translate between these worlds. They can sit with a village council and talk about bones, rivers, and genealogies. They can also sit with a credit committee and show how those same elements map to risk or long-term resilience indicators.

Marina: Explain the career path to me. Say I am a student. I study “ecological resilience auditing” under your framework. What do I actually do for work? Who pays me?

Arnie: Start at the community level. A village, a municipality, or a network of tribes commissions a resilience baseline. That includes vulnerability profiles, ecological status, and cultural sites. The intemerate auditor participates in that work. Maybe advises… but the valuation comes from the community, and the role of the auditor might be to recommend or help adjust those values, but I don’t know, maybe think of the auditor as an informed translator.

Then you have intermediary businesses. These are community-controlled entities that package projects: mangrove restoration, regenerative agriculture, small-scale energy, local health or education services. They need credible audits to access climate finance, development funds, or cooperative banks.

On the other side, you have funders. They need a pipeline of projects that are both ecologically sound and socially legitimate. They pay for audits and ongoing monitoring because that lowers their risk. Over time, auditors can work for community cooperatives, public agencies, or independent firms that specialize in intemerate verification.

Marina: So this is a whole ecosystem. Community protocols at the base. Intemerate auditors in the middle. Intermediary businesses and funds on the finance side. How does trust actually travel through that system?

Arnie: Maybe, I’m not sure. I’m not prepared to answer that question. I think a lot of options probably exist, but what you ask is going to evolve over time. I mean, to some degree, it probably already exists in a thousand different historical contexts, and if I were to name them or identify them, I would be overstepping boundaries. I mean, I have a general idea of how trust networks could evolve, but I think as soon as you define it, someone is going to develop a cryptocurrency, and it’s just going to look like shit.

Arnie: The fundamentals, however, are probably co-designed standards. Communities, auditors, and funders agree on a core set of indicators and methods, while leaving room for local variation. Each audit generates time-series data. Over five, ten, or twenty years— or even in months, you can see which communities and which auditors consistently meet or exceed resilience targets. That creates reputational capital. And then there is network verification. Auditors and communities review each other’s work. If a project in one region claims implausible gains, others can call it out based on their own experience with similar ecosystems. And that’s not to say that there are no statistical outliers, and if there are, then we shouldn’t ignore them and adjust them to the center, but we should celebrate them and acknowledge them.

Arnie: The point is that trust is not abstract. It is documented in repeated, verifiable interactions.

Marina: Where does multipolarity fit in that picture for you? From my side, I see a lot of risk. Weak governance in recipient countries, big Chinese state-owned enterprises, debt distress, and lack of transparency. I do not want to swap Western hegemony for Chinese hegemony.

Arnie: I do not want any hegemony. The point of multipolarity for me is not to replace one center with another. It is to expand the negotiating power of communities and regions.

BRICS and BRI are important because they open additional channels of credit, trade, and infrastructure investment. Otherwise, they would have to rely on the IMF, World Bank, and G7 terms. But that only helps if communities have their own accounting and auditing tools. Otherwise, they remain as colonial subjects, stuck in the accounting valuation of deals made in Washington or Brussels.

Arnie: Intemerate accounting is one way to anchor those flows in local sovereignty. Whatever the flag on the money, the audit says: here are the conditions under which we will cooperate, and here is the evidence if you violate them.

Arnie: Ten years ago, I helped to organize the Moana Nui conference, After the second conference in Berkeley, combining the various themes of trade, militarization, resources, indigeneity, and globalization, my friend Ali’itasi and I met up in one of the hotel rooms and mapped out what we call the RRMA: the Regional Regulatory Monitoring Authority, and we submitted that to the Pacific Island Forum and that is what led me to participate in the World Band Fragility Forum on SDG 16— and that was a huge eye opener. I went to the statistical meetings and it was so obvious that these were back-door capitalization systems— but anyway, I was lucky that I got to do that.

Marina: You are asking me to shift my baseline. I usually start from the idea that Western accounting is neutral and everything else is political. You are saying Western accounting is also political, and indigenous auditing makes that visible.

Arnie: Exactly. Western accounting is very good at tracking cash, liabilities, and shareholder value. It is very bad at tracking ecological depletion, unpaid care, dispossession, or spiritual harm. That is not a bug. It reflects the priorities of the economies that designed it.

Indigenous-led auditing does not claim to be neutral. It says openly that the purpose is to sustain the community, the land, and future generations. Then it applies rigorous methods to that purpose: clear protocols, measurable baselines, peer review, and data governance.

Marina: I still worry that once you plug this into big geopolitics, it gets co-opted. A bank might badge a project as “indigenous-audited” while still pushing through highways, mines, and ports that serve its strategic interests.

Arnie: Co-optation is always a risk. The safeguard is where the data sits and who can withhold it. If the community controls the underlying data and the right to say yes or no, the intemerate audit cannot be faked without breaking protocol.

It is not perfect. Neither is GAAP or IFRS. The difference is that here the primary reference point is the community’s continuity rather than the investor’s quarterly earnings.

Marina: If a young person asked you whether to study for a CPA or become an intemerate ecological resilience auditor, what would you say?

Arnie: I would say there is room for both, and the world will need the connection between them. If you become a CPA, of course, you will make an immediate income. But if you learn how ecological and social risk actually work on the ground, if you become an intemerate auditor, you would end up learning how to sit on the mat, which I think is much more valuable than sitting at the table. For one thing, you have to earn trust.

Communities will need people who can quantify resilience in a way that respects protocol and reciprocity. Investors and public agencies will need people who can translate that into contracts, covenants, and long-term obligations.

Marina: I still have reservations about BRICS and especially about China. I am not ready to trust BRI just because there is an “indigenous audit” attached to it. But I can see that what you are describing is not just mystical talk. It is a serious proposal for how to structure evidence and trust.

Arnie: Don’t dismiss it. Recognize it as a different starting point for what counts as value and who gets to define risk.

Marina: Fair. Next time you run a training or have a draft of these standards, I would like to see them. I am curious.

ANNEX

GAAP, IFRS, and SEC auditing form the core architecture of Western accounting because they support large capital markets, not because they offer a neutral or comprehensive view of value. GAAP and IFRS standardize how firms recognize revenue, assets, liabilities, and risk so investors can compare companies across jurisdictions, while SEC auditing enforces these disclosures through legal authority. Their reach comes from the scale of US and European financial systems, which makes their methods global defaults. They excel at tracking cash flows, ownership, and measurable financial risk, but they do not account for ecological depletion, cultural obligations, or intergenerational continuity unless those issues threaten profitability. Their authority is institutional and market-driven, rather than an indication that they capture the full range of what societies consider valuable.

Through the glass, darkly, the world observes its reflection in the mirrored surface of debt. Climate finance presents itself as a race to save the planet, while concurrently dragging its feet through genocide, perpetuating, and provoking war and economic destabilization with countries and/or economies that don’t align with the targets of asset management. This image is refracted through an opaque medium in which debt and data have become indistinguishable currencies. The new economy of restoration—measured in bonds, credits, and blended instruments—rests upon the same arithmetic that has long commodified crisis. The result is a system that counts environmental virtue in units of liability, and it is within this accounting paradigm that nothing moves unless data are surrendered, standardized, and securitized by those who profit from accumulation. (See annex 1)

According to the report, 88% percent of Parties now quantify their financial needs, collectively estimating almost two trillion dollars to achieve their climate goals. Yet this number does not reflect ecological repair. It represents eligibility for loans, grants, and blended finance issued through international intermediaries, of which local communities have little access to developing or controlling. The calculation itself reaffirms dependence and development aid. The majority of states identify international sources as their principal means of implementation, while domestic finance remains marginal. For the 88%, what passes for cooperation is a hierarchy of access: to debt, to rating agencies, to the terms of disclosure. The poorer the country, the greater its obligation to make itself legible through data extraction.

With the expressed aim of decolonizing accounting methodologies, Intemerate Accounting rejects this conflation of valuation. Ecological accounting begins not with credit lines but with the veracity of local data. It treats knowledge as a reciprocal asset, not as collateral. Yet within the architecture of the Paris Agreement, data are produced for creditors, not for communities. Local biostatistics, resilience measures, and ecological inventories become the raw material for global climate finance. What is called transparency is, in practice, a kind of opacity. When trust is the real basis of reciprocity and exchange, the colonial system replaces that trust with its accounting methodology, using the language of data transparency to conceal the extraction that sustains it.

Their function is to verify compliance and maintain liquidity in funds administered by asset managers. If this is transparency, it is a ghost, a spectral transparency more aligned with the hauntology of capital, as I describe in detail in another post.

Measurement, Reporting and Verification (MRV) and Enhanced Transparency Frameworks (ETF) in the Paris regime are built to evidence compliance with Nationally Determined Contributions (NDCs) and to standardize information for eligibility, disbursement, and review. The 2025 synthesis shows that 92 percent of Parties now describe domestic MRV systems, most linked to Greenhouse Gas (GHG) inventories and biennial transparency reports under the ETF; three-quarters describe formal tracking of NDC progress. These functions discipline how data is produced and shared, and they determine who qualifies for finance and on what terms.

But this is the crux of the sham.

MRV and the ETF assume that indigenous protocols and reciprocity schemes cannot be standardized, so they subordinate them to templates that serve creditors. Intemerate Accounting inverts this. Indigenous verification rooted in trust, consent, and continuous stewardship, I would argue, produces more accurate measures than distant audit frames because it binds evidence to responsibility. Any market that does not vest ownership, custody, and authorship of data in local practitioners will undervalue community resources and overvalue investor returns. Transparency without community control is spectral: an appearance of clarity that reproduces domination while claiming neutrality.

This “spectral transparency” obscures ownership and control of the underlying data, making it more performative rather than emancipatory. It only “appears” as openness while reproducing the power of those who determine what counts and who counts. That is the sense in which the visibility of MRV becomes ghostly.

The World Bank’s estimation of environmental data as a one-hundred-trillion-dollar asset is a fiction that reveals the depth of this confusion. It presumes that ecosystems can be priced in the same ledger as, for example, sovereign debt. The coincidence that global public debt approximates the same figure is not incidental. Debt and environment mirror oneanother: both are abstractions of life converted into obligations. The debt of nations sustains the liquidity of markets, while the data of ecosystems sustains the credibility of climate finance. Each exists to justify the other. The illusion of parity conceals the asymmetry of control.

To put things in perspective, the combined debt of the ACP countries is only around $4 trillion. But for many ACP countries, that debt is blood money, and it is the very real life and death to any genuine security that might be achieved if a decolonial accounting program were adopted. To be blunt, if the ACP were to tell the OECD countries that they need to pay off their $65 trillion in debt* before tackling their $4 trillion, how would the entire accounting matrix unfold so that all debt would be zeroed out? But here’s the rub: if the OECD economies continue to accumulate global environmental data, once again, the ACP, indigenous peoples, and alterity networks will be left at a disadvantage because, without owning their data, they will not be able to control intermediary markets and remain rentiers in ecological spaces they have stewarded for generations.

Imagine the United States and the OECD economies, holding the lion’s share of global debt, defining the terms under which ecological data are valued and exchanged. This is not hyperbole. Within the UN Statistical Division, the System of Environmental Economic Accounts (SEEA) is building a data reservoir that may seem benign, but when you consider that the only ones building this new accounting system are the OECD countries, with no substantive input from the Global South or from the real equity holders of global environmental data, we should not be foolish enough to equate benign with with benevolent. The architecture of SEEA encodes the same hierarchies that structure global finance. By positioning OECD institutions as the arbiters of ecological value, it transforms measurement into ownership and transparency into control. What appears as technical coordination is, in truth, the consolidation of data sovereignty within the very economies most indebted to the planet they claim to account for.

Moreover, U.S. military installations—both long-established and newly constructed under the pretext of national defense—are often situated directly above or adjacent to vital aquifers. Their presence is not incidental. These sites discharge classified chemical and radioactive pollutants into the very sources of freshwater that sustain nearby communities, while the data on contamination, remediation, and long-term risk remain hidden under security exemptions. This produces a layered form of control: polluting the resource, manufacturing scarcity, restricting access to environmental information, and consolidating that information into asset-managed databases. Within this arrangement, water becomes a dual commodity—first as a privatized physical resource, and second as data priced and traded through the same markets that determine financial derivatives. The secrecy of military pollution is not just an environmental crime; it is a data strategy that links ecological degradation to the governance of scarcity and the monetization of knowledge within the very same asset management houses that govern the different investment sectors in OECD economies. One of the dark sides of AI is how data computations, wielded by investment regimes, can turn data into trillions of assets, before the signatures providing our consent dry. (see annex 2)

So, within this context, who, really, are the external threats and actors?

Seen through this lens, the Global Stocktake is more of a ceremonial account—there is no material measurement, because there is no local market, no locally driven intermediary markets when it comes to, for example, warehousing, logistics, health care exchanges, risk pools and cooperative insurance, cultural knowledge cooperatives, mutual credit systems, procurement hubs, audit and verification clearinghouses, etc… Within traditional knowledge systems, these are all supply chain nodules that go back centuries, before neoliberalism, capitalism, and colonialism. (see annex 3)

The Global Stocktake, as understood within COP, is a perfunctory “take” without any stock.

They audit participation without altering the ownership of value. They translate local realities into universal indicators that sustain the global financial narrative. The act of reflection is itself commodified; the world is asked to gaze upon its moral image through the glass of data that others own. Nothing will be restored until that glass shatters.

Through the glass, intemerately, clarity emerges only through the grounded work of local verification, where value returns to those who produce and sustain it.

Intemerate Accounting proposes a reversal. To account intemerately is to remove the filter of debt and to see restoration as a process of restitution, but really an act of liberation, emancipation, and decolonization (LED). Value must arise from verified restoration, held within local custody, expressed in regional accounts that balance monetary factors with ecological variables. Data must serve communities first, not creditors. Only when communities control their information can finance cease to function as an instrument of enclosure and become a mechanism of reciprocity.

Through the glass,intemerately, we begin to see how reflection has been mistaken for truth. Debt has been treated as unavoidable, and data as unquestionable evidence. To see clearly requires stepping beyond the mirror of finance and the abstractions that mistake exposure for control. Clarity emerges only through the grounded work of local verification, where value returns to those who produce and sustain it.

Decolonize Accounting is a reader-supported publication. To receive new posts and support my work with a cup of coffee, consider becoming a free or paid subscriber.

Annexes:

annex 1. 1 Corinthians 13:12 teaches that our present knowledge is partial and mediated, “through a glass, darkly,” while full understanding comes only “face to face.” The Qur’an states the same epistemic limit in a different key: hearts can be sealed and veiled so that hearing and sight fail (Q 2:7; 17:45–46). Read against the Global Stocktake, these verses name a structural problem. Aggregated indicators promise vision, yet they filter reality through distant categories and institutions. What we see is a managed reflection, not a face-to-face account of restoration. An ethical stocktake would attend to the veil itself. It would replace mediated visibility with accountable proximity by centering local custody of data, consent, and community verification. Until these conditions hold, the Stocktake measures what it is designed to allow, and dismisses what the framework excludes.